In our previous articles on the subject of platforming, we made a commitment that we would discuss the situation of the banks.

Between the regulatory constraints (PSD2 in Europe, OBWG in the UK), and the desire for openness (open banking, BAAS aka Bank as a service, BAAP aka Bank as a platform), the challenges of banks are tremendous and the positions are not yet well defined in the strategies of financial institutions.

Open banking platformization

The question we are going to ask ourselves for all other industries is simple: Is it in the bank’s interest to evolve towards a business platform model? And, if so, how is it legitimate to reposition itself?

We will limit our study today to the case of historical, traditional banks, and not neobanks.

Fundamentals

Let’s look again at the fundamental assets that make a platform successful, they are few and far between:

- Trust

Above all, you need a direct customer base. Also, these customers must have a high level of trust in the platform. For example, look at how Amazon has successfully positioned itself as a marketplace platform: they have built, over time, a relationship of trust with their customers, which allows them to position themselves as a trusted third-party business between suppliers and buyers. At the smallest claim, Amazon will refund the customer or follow up on the refund or exchange of the product. The trust between the installed customer base, and the platform is the number-one asset in building a business platform. - Security

You might say security goes hand in hand with the first point, but it is essential to remember it. The infrastructure of a platform hosts personal, behavioral, and financial data. These hosting structures cannot suffer the smallest breach of security without the immediate loss of trust of the customer base. You can, therefore, understand why Amazon has built its own platform, which operates directly and now even resells as a cloud [PAAS, IAAS] to third parties. - eID

The third dimension is the ability to manage effectively digital identity and to monetize this verified identity with third parties (Facebook connect, Google Connect, AppleID, etc.).

4. Monetization

The last dimension is the possibility to make a settlement/billing, and the associated follow-ups.

So, are banks well placed?

Taking these four fundamental dimensions into consideration, we can see that big historical banks are in a favorable position to become the kings of the digital platform:

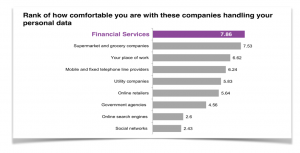

- Historically, they are best placed in the minds of their many customers who see them as a trusted organization. Look at the graph below. Banks are even further ahead of governments at this point. Customers entrust their most important assets to them, from financial assets to jewelry.

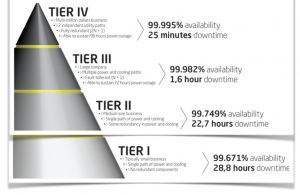

- In the area of security, all major banks operate their own Tier 4 data centers, which is the highest level of security and quality of service to date.

- Regarding identity, regulations already require banks to have extremely detailed knowledge of their customers, a verification of their identity with a process (KYC) that is very much defined by the regulators, and we can easily imagine that this verified identity represents a value for a whole ecosystem that would like to conduct commercial transactions.

- Finally, who better than banks to rely on existing and proven settlement/payment/billing systems?

All the checkboxes are ticked to ensure that the large traditional banks take a leading role in business platforming. But this is not the case. And we can legitimately ask why.

I don’t have a simple answer, but I guess anything that can be seen as an advantage in trust, security, etc., is based on long and heavy processes, which turn into a disadvantage when one has to be agile and rethink one’s traditional business to embark on a new adventure, platforming. However, today is the time for banks to make this shift.

The basis of their revenues is rapidly eroding (negative interest rates, loss of payment for individuals to the GAFA). Banks must take advantage of their cash to launch business transformation projects oriented towards the platforming and conservation of new digital values (electronic key, health data, etc.)

Instead, we see them running after the “new normality” imposed by the fintech, forgetting their fundamentals. By construction, their organizational model is incompatible with these new expectations of the digital customer relationship.

By trying to mimic the new fintech entrants on these subjects and forgetting their historical foundation that could be the basis of digital resurrection, they risk a serious blow.

Gentlemen bankers, wake up, you have extraordinary assets, don’t lose them, platformize yourself, we can help you!

Learn about open banking advantages — open banking, open API, and PSD2: A story to tell…