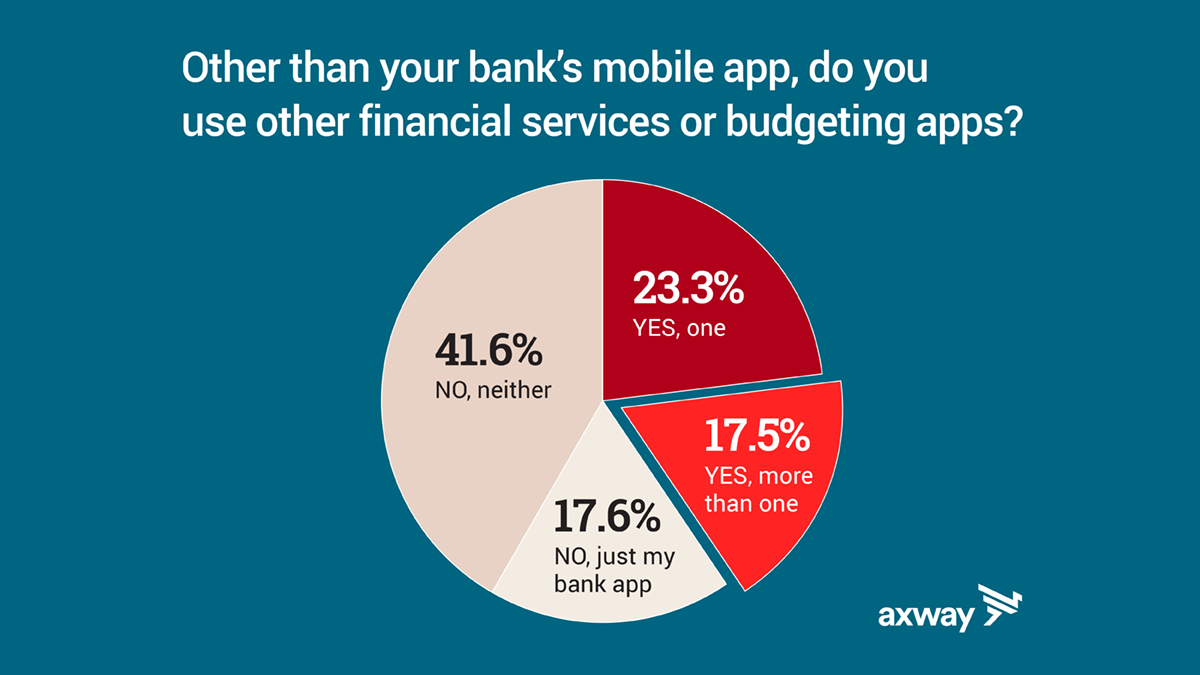

Axway’s just-released consumer survey reveals an interesting dissonance in attitudes around open banking and financial services. The 2021 survey found 81% of Americans feel their banks offer all the financial services they need in their day-to-day life — and yet, 40% say they use at least one finance or budgeting app other than their bank’s mobile app. These two statistics seem to contradict each other, but in this contradiction lies a coming shift.

The financial technology world is clearly tapping into a need and a demand — a demand which is growing fast. Despite a challenging year, global fintech investment reached $44 billion in 2020, up 14% from 2019, and half of that was raised in the U.S.

People are splitting tips and rounding up to invest, they’re getting $0 trades and specialized products for their small businesses, they’re aggregating all their financial data in one place to more easily manage it or sending money to relatives overseas in simpler and cheaper ways. Most importantly, they are doing these things outside of their traditional banks.

This indicates that we are at a transformational moment: people still trust and need their banks, but these new fintechs are offering amazing tools that people really want to use.

Open banking is the answer, but not everyone sees that yet

Open banking solves making sure traditional financial institutions and fintech can work properly — and securely — together. APIs can unlock financial data, enabling third-party software providers and banks to build new, customer-centric financial applications and services.

Here at Axway, we power open banking implementations around the world on the Amplify Platform. We believe that “Open Everything” is the key to inventing new customer experiences, building a dynamic digital ecosystem, and creating entirely new revenue streams.

At its heart, open banking is about letting people control their money. The survey shows it’s a principle people overwhelmingly support: 84% of Americans agree they should have control of their financial data, and banks should not prevent the movement of money between other financial services.

But therein lies the next contradiction: people know they like what open banking stands for and the services it can provide, but they haven’t made the connection yet to a truly open financial ecosystem.

The current sentiment is marked by interesting contradictions

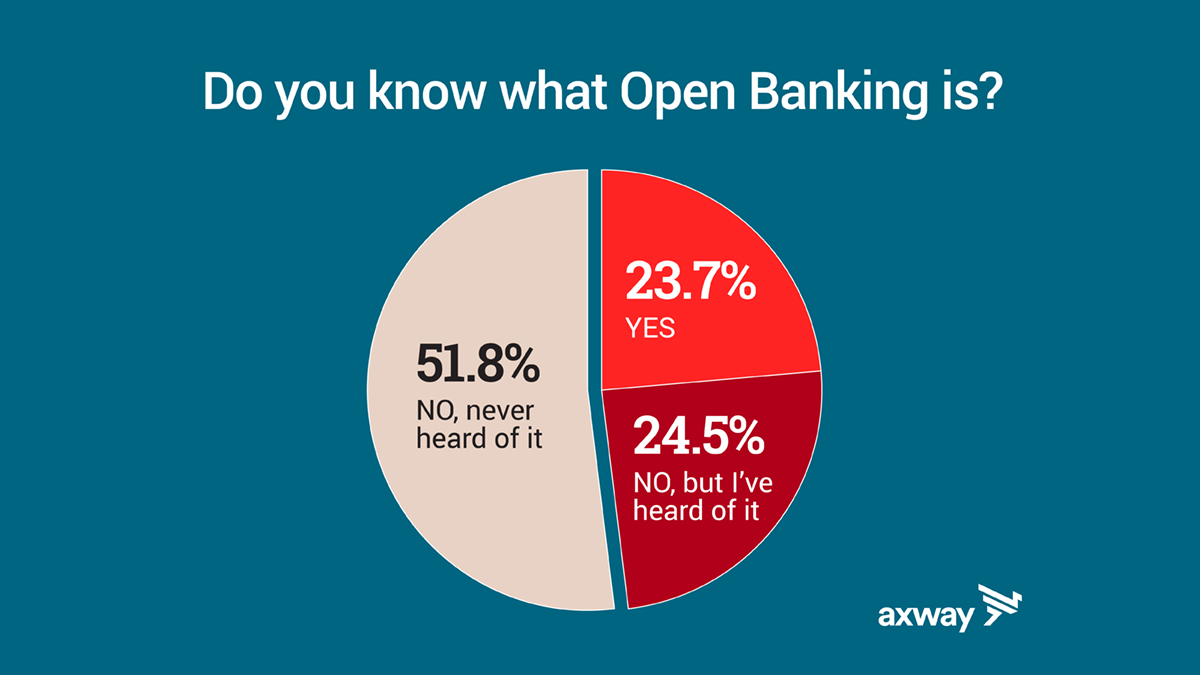

We asked Americans if they knew what open banking was, and close to half had at least heard of it. However, only half of those who had heard of it actually knew what it means and could define it.

The interesting thing is that enough people seem to know there’s something out there that involves their financial data and money moving around. It’s encouraging that there is some awareness of the term. But clearly there’s a misperception that ‘open’ means less secure.

When the concept of open banking was explained to them, half of survey respondents worried about issues surrounding constant monitoring of their financial activity (33%), losing control over access to their financial data (47%), or even financial institutions using their data against them (27%).

People hear that word “open” and think, as could be expected, “the entire world is going to be able to see my banking transactions, and that worries me!” But in fact, open banking would give people significantly more control.

Today, in the absence of open banking, you have no legal control over your financial data. There is absolutely nothing you can say to a bank regarding how they use your data once it’s in their systems. That doesn’t mean banks are abusing people’s trust, but personal ownership or rights towards financial data simply don’t exist in any meaningful way.

The mechanisms through which banks use data today are completely opaque to consumers of banking services.

Open banking is about letting you see what institutions are doing with your data and deciding whether you want to grant them permission to do it. You might authorize use or sharing of your data because you want an additional service or want to connect to a fintech, but that’s entirely within your control.

There’s a better way, and it’s also safer

Open banking puts the standards and technologies in place that make data ownership and consent possible. It also leads to better customer experiences, like greater ease in transferring money between accounts, and more innovative financial products that increase financial utility.

In the Axway survey, 21% of Americans said they had recently written themselves a check from one bank and cashed it in the other, and 16% withdrew cash and physically deposited it in their other bank. It should not have to be this way.

The existing ways of moving money around can sometimes be confusing, obtuse, or expensive. Open banking would help do away with an arbitrary institutional lock-in and make for smoother customer experiences.

Of note is that open banking is actually a more secure way of enabling the experiences many fintechs are already creating. In Canada, for example, four million Canadians use screen scraping, which is significant for a country of 35 million.

Screen-scraping is how fintech services often have to work around the lack of open data agreements to allow you to pull information from multiple accounts and conveniently view it in one place.

It means you have to provide your account passwords to the fintech service, and it can be risky — not to mention there is nothing to stop the screen-scraping fintech from re-using or even selling your data and you have no recourse.

Open banking can solve these security concerns and make all these players work together more smoothly. If financial institutions accept and embrace this new operational model, they can use APIs to become more flexible and drive new revenue by extending their reach, embedding themselves into all kinds of digital experiences.

This is only the beginning

As the world moves steadily toward an expanded financial ecosystem, as demonstrated by the continued expansion of Europe and Australia’s open banking laws in the last several years, open banking has now become a strategic imperative.

It’s not just about compliance with regulation: it’s about making sure you’re ready for the digital economy of the 21st century, opening up silos and freeing data so its rightful owner: the individual who created it can control and leverage it.

Recently, we even got a hint that the U.S. government might be considering entering the conversation: with President Biden’s executive order designed to improve competition, the White House has taken a bold step towards bringing open banking to the U.S.

The order specifically states customers should be able to “easily take their financial transaction history data to a new bank,” and that it “encourages the Consumer Financial Protection Bureau (CFPB) to issue rules allowing customers to download their banking data and take it with them.”

2024 update: Why you should act now on the CFPB proposed rule for open banking

Data portability and ownership? Sure sounds a lot like open banking, and we already know there’s an appetite for it.

51% of Americans told us they felt the growing movement towards open banking is positive, citing reasons like better financial services, comparison of offers or simplified borrowing and payments methods. And 84% of people agree with open banking’s central tenet: that they should have control of their financial data, and banks should not prevent the movement of money between other financial services.

Here’s hoping this is just the beginning of America’s journey towards true open banking.

Discover more resources for the successful adoption of APIs in financial services.